Not Too Little, Not Too Much: How to Calculate the Goldilocks of Withholding On Your W-4

Confused about what’s happening with the new W-4? You’re in good company! In 2020 the IRS changed the withholding form and now many of you are not paying enough to cover your tax, let alone get a refund. Not exactly the surprise you were looking for to welcome spring 2022.

Despite the fact that most people do encounter a W-4 form when they get a new job, not everyone understands how much it impacts their tax bill. But we’re here to explain what it is, and how to fill it out in a way that can make your tax experience a more positive one.

So what exactly is the W-4 Form?

The W-4, formally known as the “Employee’s Withholding Certificate,” is an IRS form employees used to tell employers how much tax to withhold from each paycheck. Employers use the W-4 to calculate certain payroll taxes and remit the taxes to the IRS and the state on behalf of employees. You don’t have to fill one out if you already have one on file with your employer, so it may not be something you think about from year to year. But you may want to check in on how much you are withholding and adjust it accordingly.

What’s changed?

In the past, employees could claim allowances on their W-4 to lower the amount of federal income tax withheld from their wages. The more withholding allowances an employee claimed, the less their employer would withhold from their paychecks. However, the 2017 Tax Cuts and Jobs Act overhauled a lot of tax rules, including doing away with personal exemptions. Sad! With the new W-4, you are still asked for basic personal information, but you are no longer asked for a number of allowances. Now, employees who want to lower their tax withholding must claim dependents or use a deductions worksheet.

What does this mean for you?

It’s important to fill out a Form W-4 correctly because the IRS requires people to pay taxes on their income gradually throughout the year.

If you have too little tax withheld, then you could owe a surprisingly large sum to the IRS in April, plus interest and penalties for underpaying your taxes during the year. This isn’t an ideal situation, as you may not have budgeted for such an expense during the tax season.

However, if you have too much tax withheld, then your monthly budget will be tighter than it needs to be, and we could all use a little extra money in our pockets. Also, you’ll be giving the government an interest-free loan, when you could be saving or investing that money. You won’t get your overpaid taxes back until the following year when you file your tax return and get a refund. At that point, you may feel like you’ve won the lottery and spend the money more frivolously than you would if it had been part of your monthly budget.

How do I update my W-4?

We’ve broken down this process into 5 easy steps, and only steps 1 and 5 are required for all workers!

Step 1: This is the usual personal information that identifies you and indicates whether you plan to file your taxes as a single person, a married person, or a head of household. You’ll include your name, address, filing status, and social security number. After completing this step, single filers with a simple tax situation only need to sign and date the form, and they are done. Everyone else has to take a few more steps.

Step 2: This part is for people whose circumstances indicate that they should withhold more or less than the standard amount. This applies if you have more than one job or your filing status is married filing jointly and your spouse works. To ensure you are withholding the correct amount there are three processes you can use.

Option A

Use the IRS’s online Tax Withholding Estimator and include the estimate in step 4 (explained below) when applicable.

Option B

Fill out the Multiple Jobs Worksheet, which is provided on page 3 of Form W-4, and enter the result in step 4(c), as explained below.

The IRS advises that the worksheet should be completed by only one of a married couple, the one with the higher-paying job, to end up with the most accurate withholding.

W-4 Multiple Jobs Worksheet.

When filling out the Multiple Jobs Worksheet, the first thing you will need to differentiate is whether you have two jobs (including both you and your spouse), or three, or more. If you and your spouse each have one job, then you’ll complete line 1 on the worksheet. If you have two jobs and your spouse does not work, you will also complete line 1.

To accurately fill in line 1, you’ll need to use the graphs provided on page 4 of Form W-4. These graphs are separated out by filing status, so you’ll need to select the correct graph based on how you file your taxes. The left-hand column lists dollar amounts for the higher-earning spouse, and the top row lists dollar amounts for the lower-earning spouse.

For example, let’s look at a person who is married filing jointly. Assuming Spouse A makes $80,000 per year and Spouse B makes $50,000 per year, Spouse A would need to select $8,120 (the intersection of the $80,000–$99,999 row from the left-hand column and the $50,000–$59,999 column from the top row) to fill in line 1 on the Multiple Jobs Worksheet.

2022 Form W-4 Married Filing Jointly Income Tax Table.

If you have three or more jobs combined between yourself and your spouse, then you will need to fill out the second part of the Multiple Jobs Worksheet. First, select your highest-paying job and second-highest-paying job. Use the graphs on page 4 to figure the amount to add to line 2a on page 3. This step is the same as the example above, except you’re using the second-highest-paying job as the “lower paying job.”

Next, you’ll need to add the wages from your two highest-paying jobs together. Use that figure for the “higher paying job” on the graph from page 4, while using the wages from the third job as the “lower paying job.” Enter the amount from the graph to line 2b on page 3, and add lines 2a and 2b together to complete line 2c.

For example, let’s assume Spouse A has two jobs making $50,000 and $15,000, while Spouse B has one job making $40,000. Spouse A would enter $3,520 on line 2a (the intersection of the $50,000–$59,999 row from the left-hand column and the $40,000–$49,999 column from the top row). Adding $50,000 and $40,000 together for a total of $90,000, Spouse A would enter $2,820 on line 2c (the intersection of the $80,000–$99,999 row from the left-hand column and the $10,000–$19,999 column from the top row). Adding these two amounts together results in $6,340 for line 2c.

You’ll need to enter the number of pay periods in a year at the highest-paying job on line 3 of the Multiple Jobs Worksheet—so, 12 for monthly, 26 for biweekly, or 52 for weekly. Divide the annual amount on line 1 (for two jobs) or line 2c (for three or more jobs) by the number of pay periods. Enter this figure on line 4 of the Multiple Jobs Worksheet and line 4c of the Form W-4.

Option C

Check the box in option C if there are only two jobs total for the two of you, and do the same on the W-4 for the other job. Choosing this option makes sense if both earn about the same. Otherwise, more tax may be withheld than necessary.

Step 3: This section is where you indicate the number of your children or other dependents to determine your eligibility for the Child Tax Credit and credit for other dependents. Single taxpayers who make less than $200,000—or those married filing jointly who make less than $400,000—are eligible for the Child Tax Credit.

Technically, the IRS definition of a dependent is pretty confusing (see IRS Publication 501 for details), but the short answer is that a dependent is a qualifying child or a qualifying relative who lives with you and is supported by you financially.

Multiply the number of qualifying children under age 17 by $2,000 and the number of other dependents by $500. Add the dollar sum of the two to line 3.

The Child Tax Credit and Advance Child Tax Credit Payments (which ended with the December 2021 payment) are not taxable and therefore are not relevant to the information on your W-4 form.

Step 4: This optional section allows you to indicate other reasons to withhold more or less from your paycheck. Passive income from investments, for example, may increase your annual income and the amount of taxes that you owe. Itemizing deductions may lower the amount of taxes that you owe. These may be reasons to adjust your withholding on the W-4.

In this section, the IRS asks if you want an additional amount withheld from your paycheck.

“Of course not,” you say. “You’re taking enough of my money already.”

But the information that you’ve provided in the previous sections might result in your employer withholding too little tax over the course of the year. That could land you with a big tax bill and possibly underpayment penalties and interest in April.

How do you know if this might happen? One likely cause is if you receive significant income reported on Form 1099, which is used for interest, dividends, or self-employment income on which you have not yet paid taxes. Or, you may be still working but receiving pension benefits from a previous job or Social Security retirement benefits.

Step 4 of a W-4 allows you to have additional amounts withheld by filling out one or more of the following three sections:

4(a)

If you expect to earn “non-job” income not subject to withholding, such as income from dividends or retirement accounts, enter the amount in this section.

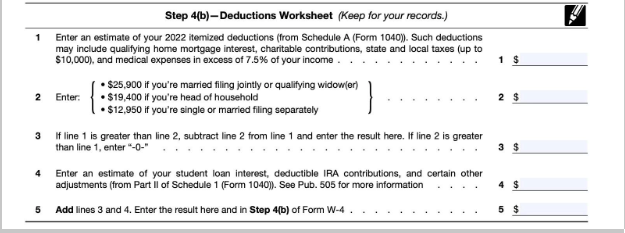

4(b)

Fill out this section if you expect to itemize your deductions and want to reduce your withholding. To estimate your deductions, use the Deductions Worksheet provided on page 3 of the W-4 form.

4(c)

This section allows you to have any additional tax that you want withheld from your pay each pay period—including any amounts from the Multiple Jobs Worksheet, as described above, if this applies to you

Step 5: Sign and Date Form W-4

The form isn’t valid until you sign it, so don’t forget!

We know this all can be overwhelming, so feel free to reach out to our tax experts to talk through it together!